Based on analysis of S&P Global environmental, social and governance data, nearly 40% of India-headquartered companies conduct physical risk assessments, and one-third of large Indian companies rate climate strategy as one of their top three material issues.

Published: August 3, 2023

A higher percentage of Indian firms compared with firms globally consider climate strategy a material issue, according to S&P Global ESG Scores raw data based on the S&P Global Corporate Sustainability Assessment (CSA).

About one-quarter of major Indian companies have a plan to adapt to the physical impacts of climate change, higher than the global average, according to S&P Global Sustainable1 analysis of 187 companies headquartered in the country and representing 85% of local market capitalization.

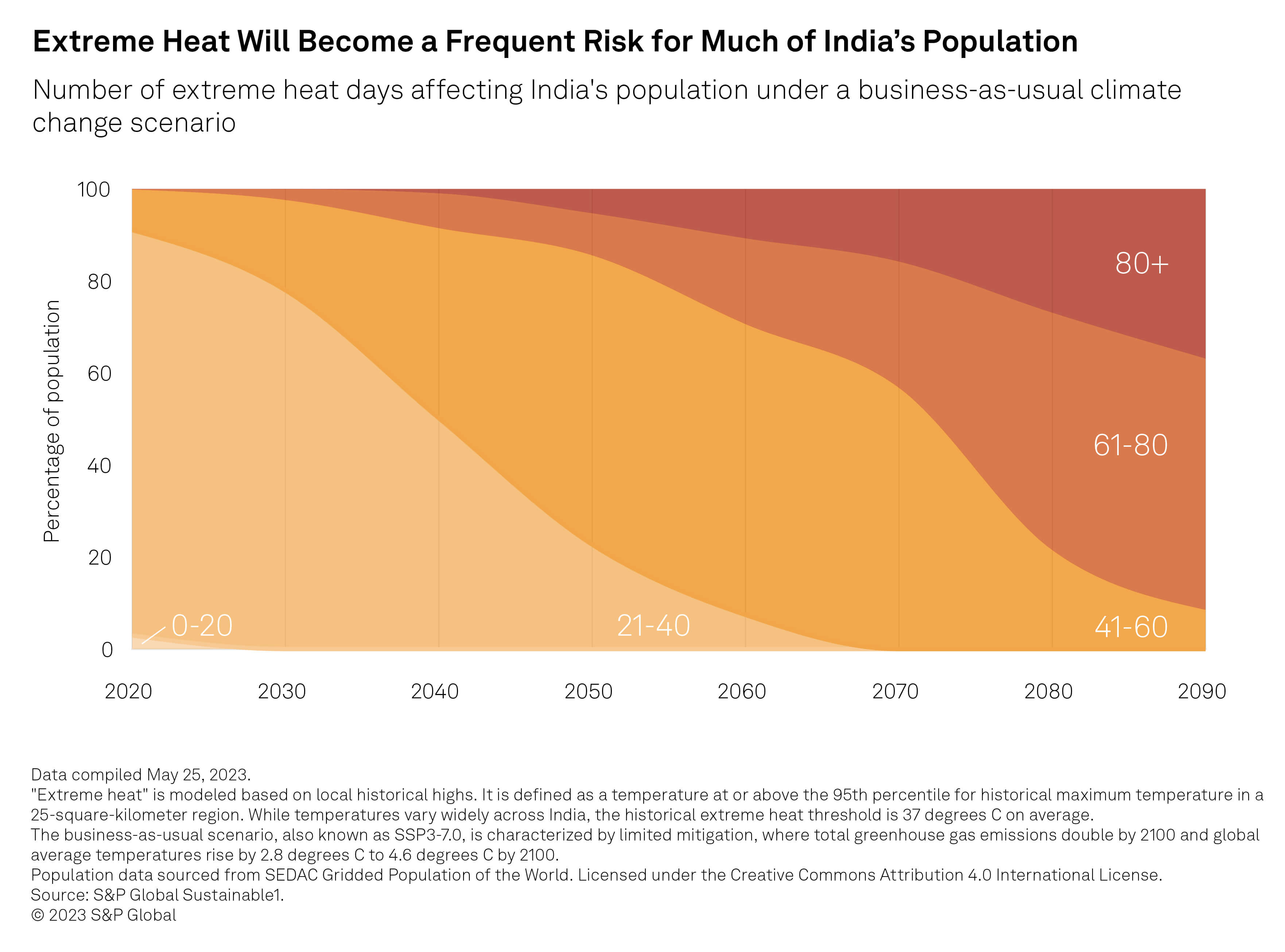

Almost all of India’s economy and population will be exposed to more frequent extreme heat by 2050, S&P Global Sustainable1 data shows.

I

n India, as in much of the world, the physical hazards of climate change are becoming more severe and more frequent. The country faces major challenges ahead from increasing heat waves and floods, which will put its economy, businesses and rapidly growing population at risk. Investment will be key to addressing these challenges, and companies will play a major role in providing the financing needed for the country’s energy transition.

Assessing physical risks and implementing adaptation plans can help companies prepare for the effects of extreme weather events on their business and the broader economy. However, companies globally need to engage in climate adaptation planning to build resilience to these hazards, research from S&P Global Sustainable1 shows. This trend holds true for Indian companies as well.

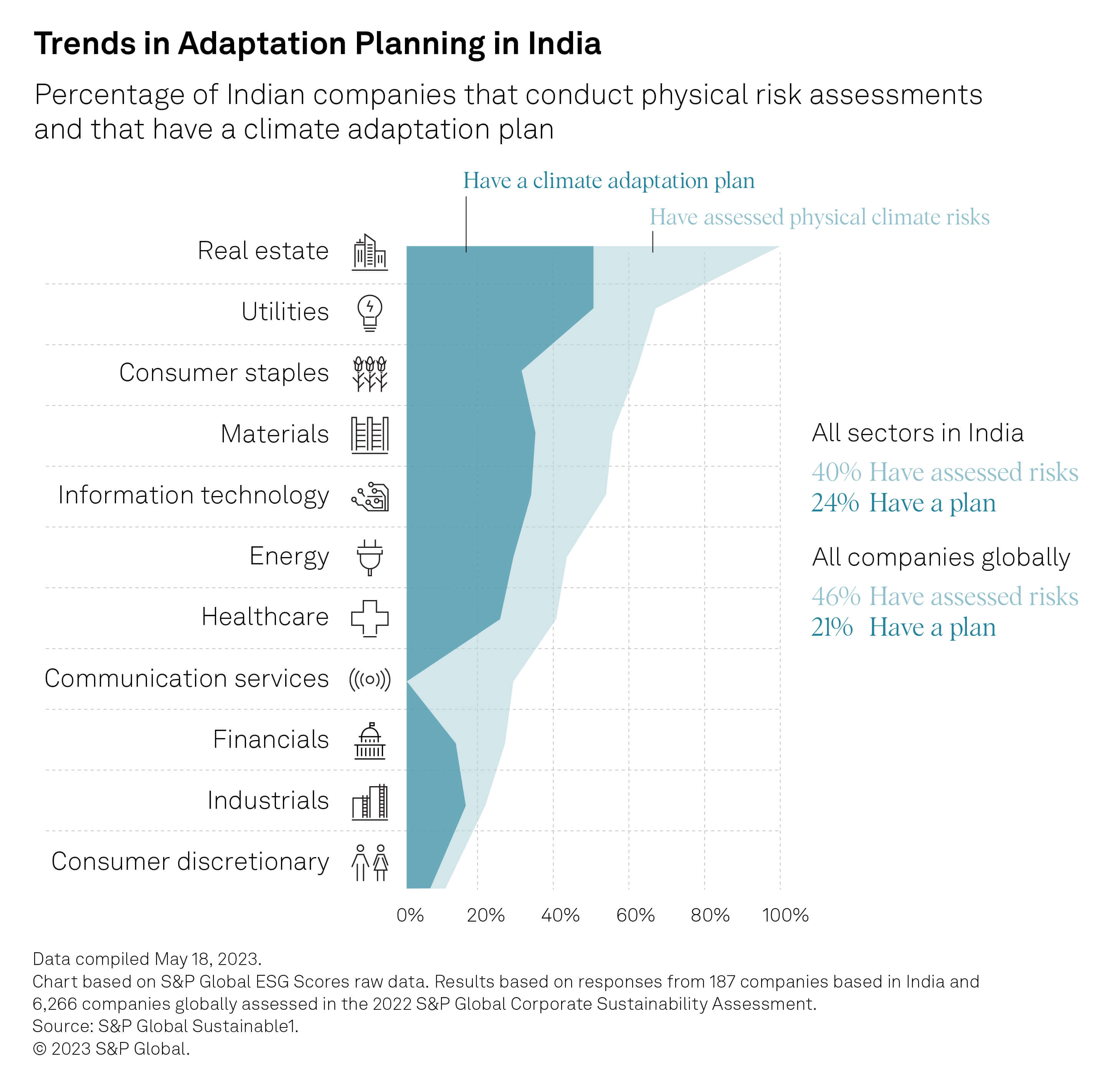

About one-quarter of Indian companies (24%) have a plan to adapt to the physical impacts of climate change, compared with the global average of 21%, according to S&P Global ESG Scores raw data, based on the 2022 S&P Global Corporate Sustainability Assessment (CSA). The universe is based on assessments of 187 companies headquartered in India, representing 85% of the nation’s market capitalization. While this is not the only signal of steps taken to mitigate climate risk, an adaptation plan is a key indicator of a company’s efforts.

S&P Global defines an adaptation plan as a plan to adapt to any climate risks across a company’s value chain that have been identified through a climate risk assessment. These can be specific climate-related mitigation plans included in wider risk assessments or separate climate-specific reports.

Utilities and real estate lead physical risk adaptation planning among the 187 Indian companies covered in the assessment, with 50% of businesses in both sectors having plans. Utilities are heavily reliant on physical infrastructure, which will be increasingly at risk of damage and disruption from storms, flooding and other climate hazards. The built environment accounts for 40% of global emissions. The Indian real estate industry has been taking steps to undertake sustainable projects that are more resilient to climate hazards. Unplanned urbanization and unregulated construction make India more vulnerable to physical hazards such as flooding, according to the World Bank.

Nearly 40% of India-headquartered companies conduct physical risk assessments, based on analysis of S&P Global environmental, social and governance data. Physical risk assessments form the basis for adaptation plans as they can show how vulnerable an organization might be to hazards such as heat waves or floods. Sectors that carry out physical risk assessments are more likely to implement physical risk adaptation plans. For example, all of the real estate companies in our analysis conduct physical risk assessments, along with about two-thirds of utility companies. These are also the sectors with the highest rates of physical risk adaptation planning.

Among consumer services companies, 28.6% in our analysis carry out physical risk assessments, but at present none have adopted adaptation plans. In consumer discretionary, 13% of companies conduct physical risk assessments and 8.7% have a plan.

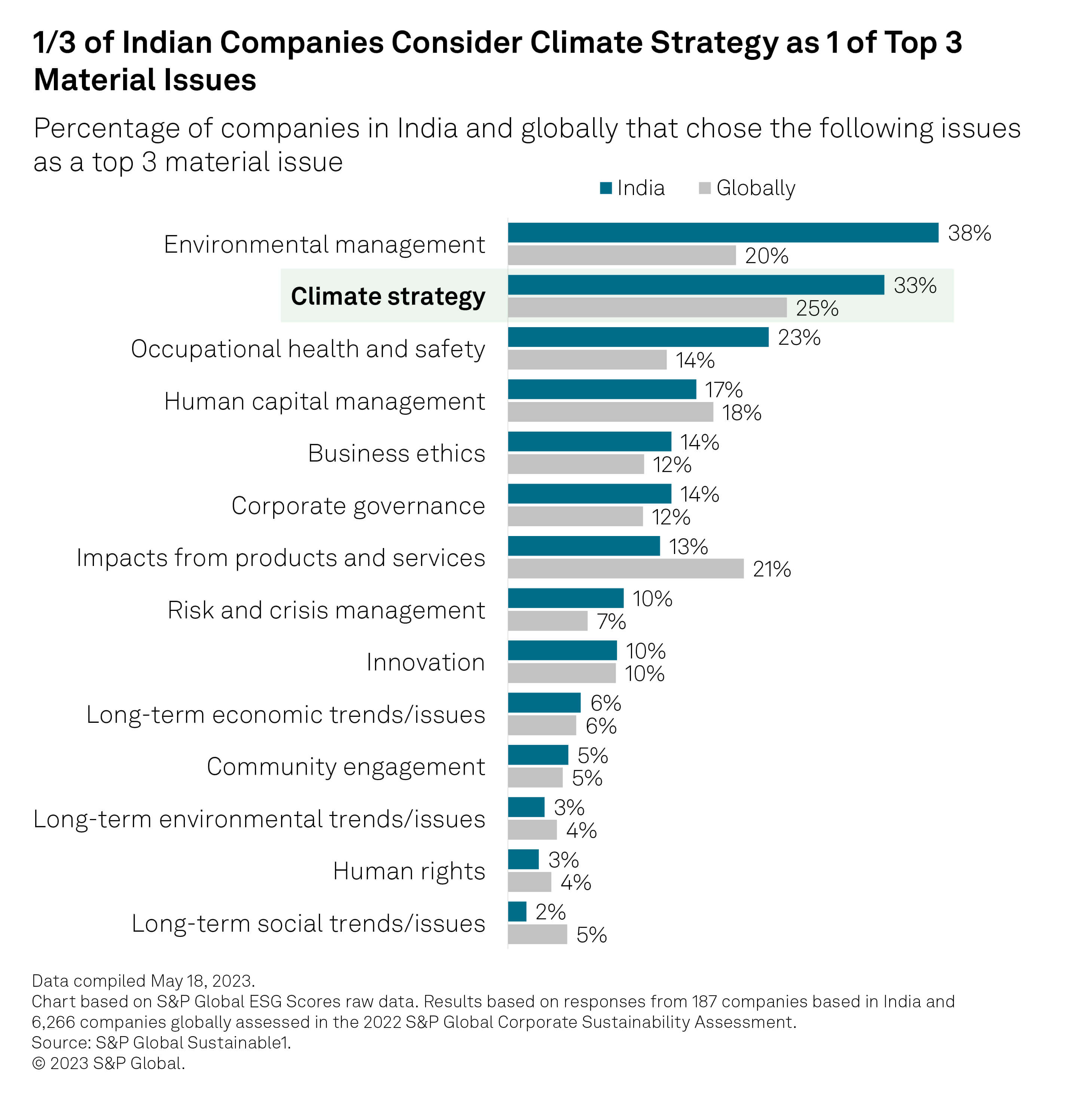

While adaptation planning and physical risk assessments are not yet widespread globally, about 33% of large Indian companies in the CSA rate climate strategy as one of their top three material issues. That surpasses the share among the 6,266 companies assessed worldwide and likely reflects the fact that India is already feeling the acute impact of physical risk hazards

Environmental management is one of the top three material issues for 38% of Indian companies in our analysis, compared with about 20% globally. The country contains 14 of the world’s 20 most-polluted cities, according to IQAir. Air pollution costs the Indian economy $95 billion per year, or 3% of GDP, consultants Dalberg Advisors, the Clean Air Fund and the Confederation of Indian Industry said in a 2021 report.

The physical hazards of climate change, such as extreme heat, can lead to power outages, increased air pollution and public health issues. This in turn results in severe health risks to the population, lower labor productivity and reduced economic growth. The country has suffered more than 24,000 heat-wave-related deaths since 1992, according to University of Cambridge researchers. The country is likely to have a greater share of its economy exposed to physical risks than peers by 2050 because of high exposure to wildfires, floods, storms and rising sea levels, S&P Global Ratings said in an April 2022 analysis.

S&P Global Sustainable1 uses the UN Intergovernmental Panel on Climate Change (IPCC) climate scenario SSP3-7.011 as a conservative representation of business-as-usual in which emissions continue to rise to the end of the century. Under this scenario, emissions are mitigated globally to some extent but continue to rise, resulting in a global average temperature increase of 2.8 degrees C to 4.6 degrees C by 2100. S&P Global Sustainable1 analysis shows that under this scenario 94% of India’s GDP and 89% of its population will be exposed to the effects of extreme heat by the end of this century.

While temperatures vary widely across India, the historical extreme heat threshold is 37 degrees C on average. About 15% of the year 2050, or 54 days, will be hotter than this average, according to S&P Global Sustainable1 data. In New Delhi, the temperature will exceed 40 degrees C for 48 days a year by the 2050s.

India also faces vulnerability from other physical risk hazards such as flooding. Power plants that rely on water could be impacted, along with offices, datacenters, warehouses, agricultural equipment and transportation. S&P Global Sustainable1 data shows that the frequency of severe flooding will increase in many parts of India by the 2090s. A severe flood is typified as a 1-in-100-year event, meaning an event where flood depths reach a level that has only occurred on average once every 100 years in the past. When looking at India, the risk of a flooding event of this severity for some fluvial areas will double, making them 1-in-50-year events by the 2090s.

Intense rainfall during the 2019 monsoon season affected 12 million people, and economic losses were about $10 billion, according to the Reserve Bank of India. The country could face annual average losses of between $132 billion and $224 billion under moderate-to-worst-case climate change scenarios, according to a report by Indian think tank Observer Research Foundation and professional services firm PwC. The country will have to raise funding for adaptation, mitigation and the management of weather-related disasters, with investment between $7.2 trillion and $12.1 trillion by 2050, the Reserve Bank of India estimated.

Globally, the sense of urgency around climate change adaptation is growing. In March 2023, the UN IPCC released a synthesis report warning that the world must act fast to reduce emissions. The IPCC in 2018 found that the world needs to achieve net-zero emissions by 2050 to limit global warming to 1.5 degrees C. India has set a goal of reaching net-zero by 2070. It plans to reduce emissions related to economic output by 45% by 2030, versus 2005 levels.

India has just surpassed mainland China as the world’s most-populous nation, and it will have to balance a number of competing priorities: providing access to affordable, reliable and clean energy to its people while mitigating the impacts of climate change. At the same time, India will play a major role internationally for the world to reach net-zero emission goals. India’s Energy Transition outlines possible strategies and actions India can take to meet these challenges.

1Intergovernmental Panel on Climate Change (2023). Sixth Assessment Report. Available at https://www.ipcc.ch/assessment-report/ar6/.

Contributors:

Hana Beckwith

ESG Specialist,

S&P Global Sustainable1

hana.beckwith@spglobal.com

Stuart Bowles

ESG Analyst,

S&P Global Sustainable1

stuart.bowles@spglobal.com

Cornis Van der Lugt

ESG Research Senior Manager,

S&P Global Sustainable1

c.van.der.lugt@spglobal.com

Rick Lord

Head of Innovation Methodology,

S&P Global Sustainable1

rick.lord@spglobal.com

Kuntal Singh

ESG Innovation and Analytics Manager,

S&P Global Sustainable1

kuntal.singh@spglobal.com

Gauri Jauhar

Consulting Executive Director,

S&P Global Sustainable1

gauri.jauhar@spglobal.com

Financed emissions are missing from many firms’ net zero plans

Adaptation planning is the next step for companies to prepare for climate risk

How the world’s largest companies depend on nature and biodiversity

How global food producers are responding to rising water stress

Next Article:

India’s Future: The Quest for High and Stable Growth

This article was authored by a cross-section of representatives from S&P Global and in certain circumstances external guest authors. The views expressed are those of the authors and do not necessarily reflect the views or positions of any entities they represent and are not necessarily reflected in the products and services those entities offer. This research is a publication of S&P Global and does not comment on current or future credit ratings or credit rating methodologies.